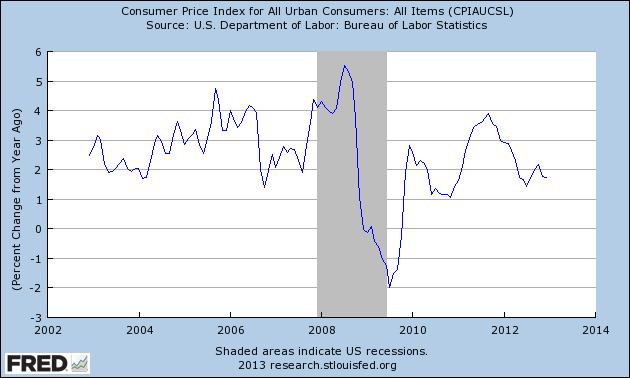

One of the most common misconceptions is that inflation risk is rising due to the growth in money supply. This misunderstanding is largely driven by the headlines of the Federal Reserve buying $85 billion of securities each month, in addition to other central banks' actions.

In normal times this level of aggressive purchases would indeed spur the money supply, but we are not in normal times. Let's review a few things:

September 2012

Federal Reserve announces it will purchase $40 billion of US Treasuries per month. At the time, growth in M2 was falling quickly, from close to 10% in June to under 6% in September. Excess reserves were falling almost 10% annually. The slowing of the velocity of M2 was beginning to moderate, declining less than 3% annually after falling around 5% during the previous twelve months.

December 2012

Federal Reserve announce it will purchase $45 billion of mortgage backed securities per month, in addition to the purchases of treasuries. M2 growth had bounced upward in October and November was appeared headed back down. Excess reserves were still declining but lower single digits annually. The velocity of money continues to decline, but at a more consistent low single digit average.

Present Day

Excess reserves are growing over 10% annually.

Thursday, May 2, 2013

Wednesday, April 17, 2013

Curtains for Monetary Policy?

In this article I argue that we may be reaching an end game for monetary policy. As economies continue to sputter and the central banks continue to pursue extraordinary measures, the question should be raised: What are we accomplishing? And, at what long-term cost?

There is little doubt the Federal Reserve's quantitative easing policy has helped bolster asset prices, especially prices for bonds, equity and houses. The U.S. stock markets sit around record highs, treasury yields are near record lows, and interest rates on mortgages are near record lows. These factors have created a "wealth effect" in which owners of these assets feel better off.

The question is: Does this asset appreciation mean we reach an "escape velocity" for the economy or does it set us up for greater volatility (ie. another burst bubble)?

Time will prove the fairest judge of this debate. But for now, maybe the biggest long lasting impact of recent monetary policy has been in the area of academia. Through Mr. Bernanke's tinkering we are learning about the limitations of monetary policy. It is becoming apparent that monetary policy has a direct impact on asset prices but the impact on labor markets and consumer spending is more indirect, and potentially dominated by other factors. Similar to a whip, Bernanke applies force to one end with the expectation of a "crack" at the other end. Will the monetary force used to lift asset prices result in a Bernanke-Jones whip-like economic snap or a Bernanke-Tube Man violation?

The declining velocity of money and slowing growth in the money supply suggest more of a tube man blowing hot hair than Indiana Jones getting the treasure (and girl). Slowing velocity and slowing monetary base growth equals slowing nominal GDP. In other words, inflation risk is declining and deflation risk is increasing, supported by weak gold prices and TIPS.

Recent economic releases continue to paint a mixed economic picture. Consumer spending appears weakening, with cash-register sales declining 0.4% in March. Consumer sentiment fell to the lowest level in nine months. Retailers are actually cutting jobs. The reasons for this weakness are varied, including rising healthcare costs consuming more of a family's budget, rising income taxes, falling mortgage refinancing activity as rates have been at a prolonged nadir, and federal sequestration.

The recent weakness in bank earnings, and the nearing end of lowering loan-loss reserves to bolster earnings, may provide a clearer picture of the strength of the economy. In an ultra low long-term rate environment it is challenging for financial companies to produce acceptable returns. Even more concerning, a research article by Robert C. Merton highlights that due to explicit and implicit government guarantees bank earnings face a "doubly convex" curve, masking the real risk to banks' earnings when the economy worsens and increasing economic volatility. So what seems like satisfactory risk controls in a normal environment can quickly deteriorate into a crisis during an economic downturn.

Central banks are raising the stakes in their battle to drive economic growth, a notion that should cause more skepticism. Most recently, Japan's central bank has committed to expand its balance sheet through asset purchases at the rate of 1% of GDP each month, potentially doubling the base money within two years. This policy is expected to continue for as long as necessary. All of this to offset a naturally deflationary environment caused by an aging population and a relatively inflexible economy. Are central banks lifting us to a recovery or simply holding on as more weight is added to a recession scenario?

Rising prices are not a major contributor with most commodity prices flat to down, including major influences like gasoline and food. Countries that have traditionally relied on commodity exports have been experiencing weakness, including Canada and Chile. In fact, with a consumer debt level to disposable income at a record level of 165% and oil revenue $6 billion below expectations, there is growing concern in Canada that the economy will continue to weaken.

In an environment in which some have characterized as a "no bad news" environment for markets, there is a deep fundamental belief that the monetary policy can cure all. In a perverse way, bad labor market statistics actually encourage the markets because the likelihood of the Fed extending its easing stance increases. Great for the asset markets but maybe not as much so for the economy, especially when growing risks of price destabilization, either inflationary or deflationary, are considered

The markets continue to skip down the path paved by the Bernanke-the-wizard's dollars. Take away that dollar-covered curtain and the picture is down right scary.

There is little doubt the Federal Reserve's quantitative easing policy has helped bolster asset prices, especially prices for bonds, equity and houses. The U.S. stock markets sit around record highs, treasury yields are near record lows, and interest rates on mortgages are near record lows. These factors have created a "wealth effect" in which owners of these assets feel better off.

The question is: Does this asset appreciation mean we reach an "escape velocity" for the economy or does it set us up for greater volatility (ie. another burst bubble)?

Time will prove the fairest judge of this debate. But for now, maybe the biggest long lasting impact of recent monetary policy has been in the area of academia. Through Mr. Bernanke's tinkering we are learning about the limitations of monetary policy. It is becoming apparent that monetary policy has a direct impact on asset prices but the impact on labor markets and consumer spending is more indirect, and potentially dominated by other factors. Similar to a whip, Bernanke applies force to one end with the expectation of a "crack" at the other end. Will the monetary force used to lift asset prices result in a Bernanke-Jones whip-like economic snap or a Bernanke-Tube Man violation?

The declining velocity of money and slowing growth in the money supply suggest more of a tube man blowing hot hair than Indiana Jones getting the treasure (and girl). Slowing velocity and slowing monetary base growth equals slowing nominal GDP. In other words, inflation risk is declining and deflation risk is increasing, supported by weak gold prices and TIPS.

Recent economic releases continue to paint a mixed economic picture. Consumer spending appears weakening, with cash-register sales declining 0.4% in March. Consumer sentiment fell to the lowest level in nine months. Retailers are actually cutting jobs. The reasons for this weakness are varied, including rising healthcare costs consuming more of a family's budget, rising income taxes, falling mortgage refinancing activity as rates have been at a prolonged nadir, and federal sequestration.

The recent weakness in bank earnings, and the nearing end of lowering loan-loss reserves to bolster earnings, may provide a clearer picture of the strength of the economy. In an ultra low long-term rate environment it is challenging for financial companies to produce acceptable returns. Even more concerning, a research article by Robert C. Merton highlights that due to explicit and implicit government guarantees bank earnings face a "doubly convex" curve, masking the real risk to banks' earnings when the economy worsens and increasing economic volatility. So what seems like satisfactory risk controls in a normal environment can quickly deteriorate into a crisis during an economic downturn.

Central banks are raising the stakes in their battle to drive economic growth, a notion that should cause more skepticism. Most recently, Japan's central bank has committed to expand its balance sheet through asset purchases at the rate of 1% of GDP each month, potentially doubling the base money within two years. This policy is expected to continue for as long as necessary. All of this to offset a naturally deflationary environment caused by an aging population and a relatively inflexible economy. Are central banks lifting us to a recovery or simply holding on as more weight is added to a recession scenario?

Rising prices are not a major contributor with most commodity prices flat to down, including major influences like gasoline and food. Countries that have traditionally relied on commodity exports have been experiencing weakness, including Canada and Chile. In fact, with a consumer debt level to disposable income at a record level of 165% and oil revenue $6 billion below expectations, there is growing concern in Canada that the economy will continue to weaken.

In an environment in which some have characterized as a "no bad news" environment for markets, there is a deep fundamental belief that the monetary policy can cure all. In a perverse way, bad labor market statistics actually encourage the markets because the likelihood of the Fed extending its easing stance increases. Great for the asset markets but maybe not as much so for the economy, especially when growing risks of price destabilization, either inflationary or deflationary, are considered

The markets continue to skip down the path paved by the Bernanke-the-wizard's dollars. Take away that dollar-covered curtain and the picture is down right scary.

Monday, February 4, 2013

Economic Growth of 4% in 2013?

A few predictions for 2013

How can I be so sure in my "prediction?" Because I believe that price stability is the largest threat to the economy, and therefore 2013 nominal GDP has such a wide potential range that predicting its growth is no better than a game of darts. Following on from my last article, the Federal Reserve has done a masterful job so far at balancing the fundamental deflationary forces in the economy with the inflationary forces of the QE strategy. But, their path is narrowing and their control loosening, in my opinion.

Fundamental deflationary forces are coming from trends like:

Hold onto your hats because I believe the markets have been lulled into a feeling of "the Fed has our backs," allowing that silent killer called risk to creep further into our economy, likely producing large price swings in my view. Let us just hope that Mr. Bernanke is as cunning and well-equipped as the Roadrunner when the silent killer of risk sneaks up on investors.

- Global economic growth of 3.5%, accelerating from 3.2% in 2012 (Source: IMF)

- US economic growth of 2.0%, accelerating to 3.0% in 2014 (Source: IMF)

- US Retail sales growth of 3.4%, with on-line sales growth between 9% to 12% (Source: NFR)

How can I be so sure in my "prediction?" Because I believe that price stability is the largest threat to the economy, and therefore 2013 nominal GDP has such a wide potential range that predicting its growth is no better than a game of darts. Following on from my last article, the Federal Reserve has done a masterful job so far at balancing the fundamental deflationary forces in the economy with the inflationary forces of the QE strategy. But, their path is narrowing and their control loosening, in my opinion.

Fundamental deflationary forces are coming from trends like:

- Technology advancement

- Excess capital in industries like retail

- Mis-allocated capital as banks postpone write-offs of under-performing loans

- A leveraged consumer based on debt to income

- Flat real income

- Rising taxes paid on income, reducing disposable income

- More controlled government spending, especially in Europe and wind-down of wars

- Raising income after interest expense through lower interest rates

- Encouraging capital investment by lowering the cost of capital

- Inflating both financial and tangible asset prices through direct purchases and lower financing

Hold onto your hats because I believe the markets have been lulled into a feeling of "the Fed has our backs," allowing that silent killer called risk to creep further into our economy, likely producing large price swings in my view. Let us just hope that Mr. Bernanke is as cunning and well-equipped as the Roadrunner when the silent killer of risk sneaks up on investors.

Wednesday, January 23, 2013

Federal Reserve On Road to Vanishing Point?

Vanishing Point - In art, the point on the horizon line at which

any two or more parallel lines seem to meet.

For this article, the space between the two lines represents the road of Quantitative Easing with price stability, the space to the left - deflation, and the space to the right - inflation. The longer the Federal reserve extends QE into the future, the harder it becomes to maintain price stability, ultimately proving unsustainable at the vanishing point. Our position remains fixed as we watch the Fed drive down the road.

Deflationary - Commodities, Wage-Price

Neutral - Currency, Fiat, Good and Services

Inflationary - Financial Assets, Tangible Assets

In this entry I again borrow the framework developed by A. Gary Schilling on inflation to breakdown the trends and hopefully glean a bit more insight into the future. His framework breaks down inflationary/ deflationary pressures into seven areas, which are commodity, wage-price, financial assets, tangible assets, currency, fiat, and goods and services.

Commodity - Deflationary

Wage-Price - Deflationary, but Possibly Recovering

If income growth is flat-to-down, then the only way demand for goods and services can increase is if either debt levels go up (savings go down), or prices go down. Not surprisingly, the radio station WBUR highlighted that breaks in income streams has increasingly contributed to greater financial difficulty amongst consumers.

Indeed, total consumer credit has steadily increased over the past couple years. The main driver of the growth in consumer credit is non-revolving credit, for credit for categories like automobiles, education. As total credit per capita increases, and income remains stagnant, the purchasing power of the consumer declines unless interest rates continue to decline. Alternatively, for a period of time consumption can continue if asset prices are increasing, enabling cash infusions from rising equity in homes and other assets. While debt continues to rise, I believe we are nearing the end game of both falling interest rates and rising home equity.

Financial Assets - Inflationary

Tangible Assets - Inflationary

House prices have been rising, and expectations about the rate of growth have been rising over the six months. This rise in expectations is likely the direct result of the Federal reserve purchasing mortgage-backed securities, pushing mortgage rates lower. Lower rates mean a person can afford to pay more for a house with the same income level. If banks loosen lending standards then the trend in housing prices may accelerate higher as another housing bubble is inflated.

If major banks like Bank of America begin to aggressively go after new lending business then this category may provide a major inflationary force in the economy as banks draw down reserves in order to make loans, increasing the money multiplier and thus the amount of money in circulation.

Currency - Neutral

The US dollar continues to hold up fairly well relative to most other major currencies. This resilience is largely due to the aggressive monetary policies by most foreign central banks, although there is some puzzlement. In addition, the large reserves held by banks has so far reduced the multiplier effect, and thus the actual amount of money in circulation is not nearly as high as the potential. The potential inflationary force of a weaker dollar is likely held in check so long as the US dollar holds its value relative to other major currencies and banks remain conservative with their reserves.

How the debate about the overall role of government plays out likely determines whether this swings inflationary or deflationary. If the gridlock has accomplished anything, it has allowed the status quo to remain in place, neither applying further inflationary pressures through growing deficits nor swinging to deflationary pressures through austerity measures.

Clearly the Republicans prefer the road of austerity through reduced spending, although have accepted limited tax increases to avoid the "fiscal cliff." As we have seen in Europe, this path likely causes an economic slowdown in the near-term with deflationary forces. The Democrats don't want to cut spending and seem a little more accepting of deficit spending in order to spur economic growth, although higher taxes are clearly a part of their argument.

Across the Pacific is Japan, which has pursued endless rounds of stimulus to drive economic growth, only to pile national debt up to 2.5x GDP. Japan has been described as "a fly looking for a windshield," splat is only a matter of time with an aging population and mounting debt. Across the Atlantic is Europe, which has been taking its medicine through more austere measures and seen GDP growth fall. So long as the social and political structures remain in place, Europe should emerge stronger in the long run after a painful retrenchment.

If the "grand bargain" becomes additional higher taxes coupled with lower spending, then this segment swings definitively deflationary. If spending is not cut, and even increased to stimulate the economy, then this segment applies inflationary forces to the economy. More than likely, since the deficit has been trending down, the government agrees on moderate spending cuts. Simply reducing the spending on the war effort should be considered deflationary. Of course, Congress may not increase the debt ceiling and federal spending in indiscriminately and severely cut.

Goods and Services - Neutral

The combination of flat income and rising non-revolving debt balances leaves weaker consumer spending on items typically purchased with credit cards, either discretionary or non-discretionary. It is possible that more aggressive mortgage lending practices by banks may enable home prices to rise, thus providing home owners with larger equity balances with which to spend on goods and services. However, I fear that driver would only lead to another economic shock as US consumers are already tapping 401k balances to pay monthly bills.

Has the supply of retail declined, thus enabling a rise in prices due to lessening competition? The answer is simply "no." If anything, the American consumer remains over-supplied with stores, as highlighted by the recent weakness in retail REITs focused on strip malls. This over-supply of retail outlets reduces pricing power amongst retailers and provides a deflationary force to the economy. Lower mortgage payments through re-financing and tepid economic growth have so far kept the supply-demand dynamics in balance.

AIER's EPI - Everyday Price Index

Friday, January 11, 2013

America the Producer?

In my last article I highlighted the following:

What I do find interesting is an apparent shift in manufacturing between goods produced domestically versus overseas. Due to a number of economic forces, both macro and micro, there is the beginning of a shift towards domestic manufacturing, in my opinion. Numerous individuals have argued this trend recently, highlighted by Charles Fishman in the December edition of The Atlantic. Indeed, after manufacturing output rose 10% in the first quarter of 2012 the trumpets sounded about America's manufacturing resurrection, only to fall flat for the remainder of the year. So this trend is by no means certain and definitely not smooth. With that said, I plan to explore the argument further.

Macro forces pushing a shift away from overseas to more domestic manufacturing include:

Macro forces paired with fundamental business interests should eventually make for a powerful trend, in my view. Furthermore, the President is also focused on improving the manufacturing capabilities of the country, and thus political interests are aligned with economic trends. Finally, the on-going efforts of the Federal Reserve likely continues to weaken the US dollar over the long-term, adding further support to moving manufacturing back within domestic borders.

So there appears a fairly complete argument driving the growth of domestic manufacturing above GDP growth. The key phrase is "above GDP growth."

The consensus seems to tilt towards healthy GDP growth in 2013, driving favorable earnings growth. The key assumption supporting these views, in my view, is price stability. Given the Federal Reserve's decent track record over the past few years to balancing the deflationary and inflationary forces in the economy (where I have been wrong in my investment thesis), I believe assuming price stability in 2013 is the easy argument. However, changes in fiscal policy and increasing discord within the Federal Reserve may result in more volatile prices going forward. In the next few articles I plan to look into the following topics:

(1) The assumption of price stability

(2) Expected economic growth

(3) Interesting companies likely benefiting from domestic manufacturing

- The Bush-era lower taxes have added a general stimulus to the economy, enabling individuals to purchase more products and services because of a higher after-tax income.

- The larger government outlays as a percentage of GDP have driven growth rates above what is naturally sustainable in segments like defense and construction; and has enabled a woefully inefficient healthcare industry rife with fraud and over-billing.

- The aggressive monetary policies that have fueled falling interest rates have added significant stimulus to the economy, especially in industries requiring debt financing like housing and autos.

What I do find interesting is an apparent shift in manufacturing between goods produced domestically versus overseas. Due to a number of economic forces, both macro and micro, there is the beginning of a shift towards domestic manufacturing, in my opinion. Numerous individuals have argued this trend recently, highlighted by Charles Fishman in the December edition of The Atlantic. Indeed, after manufacturing output rose 10% in the first quarter of 2012 the trumpets sounded about America's manufacturing resurrection, only to fall flat for the remainder of the year. So this trend is by no means certain and definitely not smooth. With that said, I plan to explore the argument further.

Macro forces pushing a shift away from overseas to more domestic manufacturing include:

- Higher oil prices, increasing shipping costs

- Lower natural gas prices in the US, reducing domestic manufacturing costs

- Rising China wages, which have increased five-fold since 2000 in US dollars

- Slack US labor markets and weakened unions in the US, enabling lower domestic labor costs

- Rising US labor productivity, enabling lower domestic labor costs

- Falling dollar relative to China Yuan, making Chinese products more expensive

Macro forces paired with fundamental business interests should eventually make for a powerful trend, in my view. Furthermore, the President is also focused on improving the manufacturing capabilities of the country, and thus political interests are aligned with economic trends. Finally, the on-going efforts of the Federal Reserve likely continues to weaken the US dollar over the long-term, adding further support to moving manufacturing back within domestic borders.

So there appears a fairly complete argument driving the growth of domestic manufacturing above GDP growth. The key phrase is "above GDP growth."

The consensus seems to tilt towards healthy GDP growth in 2013, driving favorable earnings growth. The key assumption supporting these views, in my view, is price stability. Given the Federal Reserve's decent track record over the past few years to balancing the deflationary and inflationary forces in the economy (where I have been wrong in my investment thesis), I believe assuming price stability in 2013 is the easy argument. However, changes in fiscal policy and increasing discord within the Federal Reserve may result in more volatile prices going forward. In the next few articles I plan to look into the following topics:

(1) The assumption of price stability

(2) Expected economic growth

(3) Interesting companies likely benefiting from domestic manufacturing

Tuesday, December 18, 2012

Forget Fiscal Cliff! Can the Economy Grow in Five Years Without Government Stimulus?

I don't know about you, but the hysteria about the fiscal cliff is beginning to really rub me raw. It is not so much the politicians doing their dance. It is instead the distraction from the larger fundamental question of: "What is right for the long-term health of the economy?"

After a big step back, let's consider what deficit spending has meant to the economy.

The amount of taxes paid, as a percentage of GDP, has declined almost 5% of GDP to 15.8%. In other words, instead of paying money to the government, individuals have been purchasing goods and services, a stimulant for the economy. Secondly, government outlays have increased over 6% of GDP to 24.3%. A significant stimulant to the economy has been higher government spending, especially in the area of healthcare.

One can argue that these figures suggest more stimulus is needed in order to avoid an economic slowdown. Indeed, there are economists on the left-side of the spectrum advocating up to $2 trillion of additional stimulus spending in order to grow the "denominator," or GDP. The basis of the argument is that cutting the government deficit produces a 1-to-1 reduction in the private surplus, hurting the economy as witnessed in Europe under austerity measures. Yes, we are talking defined formulas for calculating GDP. Also, intuitively it makes sense that slowing government spending or raising taxes will be a drag on the economy, just as the opposite was true during the last decade.

Source: New Economic Perspectives

Source: New Economic Perspectives

However, this raises the philosophical question of whether the government should be the main driver of economic growth for an extended period of time. The government can obviously drive growth, but when pursued for a decade how does this type of growth driver pervert private economic activity? President Obama has maintained budget deficits in excess of 7% of GDP during his term in office. While this has helped avoid a more catastrophic depression, I fear it is also increasing systemic risk as companies increasingly rely on both government spending and lower income and capital gains taxes, either directly or indirectly.

Where I respectively disagree is sustainability of these policies. Economists advocating stimulus spending generally argue that by growing GDP through deficits, the economy can reach a self-perpetuating growth rate, at which point the government can remove stimulus spending and on-going growth can then pay down the debt. Based on this theory, you would think after 4 years of historically high deficits the economy would have performed better. In fact, the only period in the last 10 years of fiscal stimulus that has approached "normal" economic activity was the result of an inflating housing bubble that proved short lived. I suppose an ever increasing deficit and increasingly aggressive monetary policy can keep the economy growing, but there may be a diminishing impact on GDP growth as inefficiencies in the economy are allowed to remain.

The budget deficit as a percentage of GDP has been 10.1%, 9.0%, 8.7% and 7.0% for 2009 through 2012, respectively. To put this in perspective, the largest budget deficits since WWII were a little over 5%, which only happened twice. In 2013, the budget deficit is forecast between 5.5% to 6.0%.

Again, let's review some numbers:

Why does the US benefit from ultra-low interest rates while other countries with a slightly higher debt-to-GDP have interest rates spike upwards? One of the main reason, in my opinion, is because of the Fed's bond buying. However, the size and strength of the US economy, a focus mostly on public debt, falling debt service payments, and the view of the dollar as a safe currency play important roles. But, the disparity in interest rates has caused some head-scratching. I believe my Sagflation theory helps to explain this issue through the combination of fundamental deflationary forces offset by expansionary monetary policies, both of which are pushing interest rates lower.

So debt levels have been rising. At what level does the bond market pull back from US debt is very much debatable. I will leave it by stating the obvious, the higher the leverage ratio the less forgiving is the bond market if the economy slows. Stimulative policies that raise the leverage ratio increase the risk of interest rates spiking should the economy slow before the debt can be reduced.

Why I Continue to Remain Bearish

Returning to two points made previously, and adding one more. Since 2000, the following has happened in the economy:

The larger government outlays as a percentage of GDP have driven growth rates above what is naturally sustainable in segments like defense and construction; and has enabled a woefully inefficient healthcare industry rife with fraud and over-billing. The growth rates in these industries likely moderate, although healthcare may prove more resilient given the changes to the healthcare laws.

The falling interest rates have added significant stimulus to the economy, especially in industries requiring debt financing like housing and autos. Not surprisingly, both the housing market and auto industry has enjoyed a lift as the Fed aggressively purchases treasuries and mortgage-backed securities.

The critical question, in my mind, and the one everyone is fighting over is this:

Is the economy structurally efficient for the long-term?

Hard to answer this question, but I think the fundamental deflationary forces, shadowed by excessive bank reserves, hint at over-supply and poor returns in many industries. Structurally the tax code is inefficient and this constant whining from business leaders about "uncertainty" in Washington hints of businesses too closely tied to the government and its policies. Finally, the rising amount of poorly written regulation as the government reacts to crises is likely having a cooling effect on the economy.

Mr. Bernanke can keep the growth engine bouncing along as the Fed's balance sheet now exceeds $3 trillion, and in many ways he is doing what is necessary to avoid a deflationary death spiral. But, until the government enables the economy to become more efficient I believe we are doomed to Stagflation.

So while the federal government pursues stimulative measures the markets likely respond favorably. These policies could continue throughout President Obama's term in office. However, the exit of these policies becomes riskier as the debt balance rises and the Federal Reserve's balance sheet inflates. For a fundamental analyst, it is tough to swallow any company-specific analysis when the foundation of the economy seems softer and riskier than ever before.

After a big step back, let's consider what deficit spending has meant to the economy.

| % of GDP | 2000 | 2012 |

| Total Government Receipts | 20.6% | 15.8% |

| Total Government Outlays | 18.2% | 24.3% |

The amount of taxes paid, as a percentage of GDP, has declined almost 5% of GDP to 15.8%. In other words, instead of paying money to the government, individuals have been purchasing goods and services, a stimulant for the economy. Secondly, government outlays have increased over 6% of GDP to 24.3%. A significant stimulant to the economy has been higher government spending, especially in the area of healthcare.

One can argue that these figures suggest more stimulus is needed in order to avoid an economic slowdown. Indeed, there are economists on the left-side of the spectrum advocating up to $2 trillion of additional stimulus spending in order to grow the "denominator," or GDP. The basis of the argument is that cutting the government deficit produces a 1-to-1 reduction in the private surplus, hurting the economy as witnessed in Europe under austerity measures. Yes, we are talking defined formulas for calculating GDP. Also, intuitively it makes sense that slowing government spending or raising taxes will be a drag on the economy, just as the opposite was true during the last decade.

However, this raises the philosophical question of whether the government should be the main driver of economic growth for an extended period of time. The government can obviously drive growth, but when pursued for a decade how does this type of growth driver pervert private economic activity? President Obama has maintained budget deficits in excess of 7% of GDP during his term in office. While this has helped avoid a more catastrophic depression, I fear it is also increasing systemic risk as companies increasingly rely on both government spending and lower income and capital gains taxes, either directly or indirectly.

Where I respectively disagree is sustainability of these policies. Economists advocating stimulus spending generally argue that by growing GDP through deficits, the economy can reach a self-perpetuating growth rate, at which point the government can remove stimulus spending and on-going growth can then pay down the debt. Based on this theory, you would think after 4 years of historically high deficits the economy would have performed better. In fact, the only period in the last 10 years of fiscal stimulus that has approached "normal" economic activity was the result of an inflating housing bubble that proved short lived. I suppose an ever increasing deficit and increasingly aggressive monetary policy can keep the economy growing, but there may be a diminishing impact on GDP growth as inefficiencies in the economy are allowed to remain.

The budget deficit as a percentage of GDP has been 10.1%, 9.0%, 8.7% and 7.0% for 2009 through 2012, respectively. To put this in perspective, the largest budget deficits since WWII were a little over 5%, which only happened twice. In 2013, the budget deficit is forecast between 5.5% to 6.0%.

Again, let's review some numbers:

- US Debt Held by Public - $11.5 trillion (~ 75% of GDP)

- US Debt Outstanding - $16.3 trillion (Greater than 100% of GDP)

- Estimated US Debt Outstanding 2016 - $22.8 trillion (~ 150% of GDP)

- Total Liabilities of US Government (Soc Sec, Medicare, Govt pensions) - $86.8 trillion (550% of GDP)

Why does the US benefit from ultra-low interest rates while other countries with a slightly higher debt-to-GDP have interest rates spike upwards? One of the main reason, in my opinion, is because of the Fed's bond buying. However, the size and strength of the US economy, a focus mostly on public debt, falling debt service payments, and the view of the dollar as a safe currency play important roles. But, the disparity in interest rates has caused some head-scratching. I believe my Sagflation theory helps to explain this issue through the combination of fundamental deflationary forces offset by expansionary monetary policies, both of which are pushing interest rates lower.

So debt levels have been rising. At what level does the bond market pull back from US debt is very much debatable. I will leave it by stating the obvious, the higher the leverage ratio the less forgiving is the bond market if the economy slows. Stimulative policies that raise the leverage ratio increase the risk of interest rates spiking should the economy slow before the debt can be reduced.

Why I Continue to Remain Bearish

Returning to two points made previously, and adding one more. Since 2000, the following has happened in the economy:

- Taxes paid, as a percentage of GDP, has declined almost 5% of GDP to 15.8%.

- Government outlays have increased over 6% of GDP to 24.3%.

- Interest rates on 10-Year Treasuries from around 6% to about 1.5%.

The larger government outlays as a percentage of GDP have driven growth rates above what is naturally sustainable in segments like defense and construction; and has enabled a woefully inefficient healthcare industry rife with fraud and over-billing. The growth rates in these industries likely moderate, although healthcare may prove more resilient given the changes to the healthcare laws.

The falling interest rates have added significant stimulus to the economy, especially in industries requiring debt financing like housing and autos. Not surprisingly, both the housing market and auto industry has enjoyed a lift as the Fed aggressively purchases treasuries and mortgage-backed securities.

The critical question, in my mind, and the one everyone is fighting over is this:

Is the economy structurally efficient for the long-term?

Hard to answer this question, but I think the fundamental deflationary forces, shadowed by excessive bank reserves, hint at over-supply and poor returns in many industries. Structurally the tax code is inefficient and this constant whining from business leaders about "uncertainty" in Washington hints of businesses too closely tied to the government and its policies. Finally, the rising amount of poorly written regulation as the government reacts to crises is likely having a cooling effect on the economy.

Mr. Bernanke can keep the growth engine bouncing along as the Fed's balance sheet now exceeds $3 trillion, and in many ways he is doing what is necessary to avoid a deflationary death spiral. But, until the government enables the economy to become more efficient I believe we are doomed to Stagflation.

So while the federal government pursues stimulative measures the markets likely respond favorably. These policies could continue throughout President Obama's term in office. However, the exit of these policies becomes riskier as the debt balance rises and the Federal Reserve's balance sheet inflates. For a fundamental analyst, it is tough to swallow any company-specific analysis when the foundation of the economy seems softer and riskier than ever before.

Wednesday, November 14, 2012

The Nose in the Book Penalty

Last year, in the run-up to the debt ceiling, I wrote how the Democrats were advocating a pro-inflation policy of stimulus while Republicans were advocating a pro-deflation policy of austerity. The outcome was ultimately a stalemate that led to the status quo, enabling on-going stimulus deficit spending combined with monetary easing.

Roll the clock forward almost 18 months and the national debt has continued to climb, the economy enjoyed a short-term spurt, and the economic outlook is darkening. So much for the stimulus of another $1 trillion deficit in 2012. The Democrats now appear to be second-guessing the stimulus argument, instead encouraging more of a focus on reducing the deficit. At least the two sides are now focusing on the single largest controllable factor.

Now the argument has shifted from deficit spending versus austerity to what type of austerity: higher tax collections or lower spending. While good because DC is slowly spiraling in on confronting the core problem, it is scary because austerity means likely pain. Put differently, the debate is now over who feels the most chilled by austerity.

Not surprisingly, the argument has quickly devolved into a type of class warfare. The Republicans clearly defending the rich through lower taxes and the Democrats clearly defending the poor through protection of entitlements. In the cross hairs is the middle class, who could feel the pain of both higher taxes and reduced entitlements. Thus the debate over which plan protects the middle class.

From here there are three defined paths, the Democrat path of higher tax rates with minimal entitlement cuts, the Republican path of significant cuts to entitlement spending and minimal tax increases, and the "kick the can down the road" solution our leaders love so much. Given that the President believes he received a voter mandate for higher taxes and the House Republicans believe they have a mandate to cut entitlements, the chances of compromise seem dim. The only real obstacle to the final path is the fiscal cliff, which seems to look more and more enticing to politicians as they struggle (or simply refuse) to compromise.

Ultimately I believe we need to "pay the piper," most likely through higher taxes AND meaningful entitlement cuts. Compromise must happen. But, since our politicians seem incapable of serious and intelligent compromises over a path out of our mess, we are likely to choose the least thoughtful and most disruptive path of the fiscal cliff. Yet should we go over the cliff we likely continue to have a deficit of over half a trillion dollars (assuming interest rates remain low) due to the sheer size of the problem. Maybe after going over the cliff our voter-elected partisan leaders will get down to actually figuring out some compromises.

If only there was a "nose in the book penalty" for our politicians who refuse to compromise...

Roll the clock forward almost 18 months and the national debt has continued to climb, the economy enjoyed a short-term spurt, and the economic outlook is darkening. So much for the stimulus of another $1 trillion deficit in 2012. The Democrats now appear to be second-guessing the stimulus argument, instead encouraging more of a focus on reducing the deficit. At least the two sides are now focusing on the single largest controllable factor.

Now the argument has shifted from deficit spending versus austerity to what type of austerity: higher tax collections or lower spending. While good because DC is slowly spiraling in on confronting the core problem, it is scary because austerity means likely pain. Put differently, the debate is now over who feels the most chilled by austerity.

Not surprisingly, the argument has quickly devolved into a type of class warfare. The Republicans clearly defending the rich through lower taxes and the Democrats clearly defending the poor through protection of entitlements. In the cross hairs is the middle class, who could feel the pain of both higher taxes and reduced entitlements. Thus the debate over which plan protects the middle class.

From here there are three defined paths, the Democrat path of higher tax rates with minimal entitlement cuts, the Republican path of significant cuts to entitlement spending and minimal tax increases, and the "kick the can down the road" solution our leaders love so much. Given that the President believes he received a voter mandate for higher taxes and the House Republicans believe they have a mandate to cut entitlements, the chances of compromise seem dim. The only real obstacle to the final path is the fiscal cliff, which seems to look more and more enticing to politicians as they struggle (or simply refuse) to compromise.

Ultimately I believe we need to "pay the piper," most likely through higher taxes AND meaningful entitlement cuts. Compromise must happen. But, since our politicians seem incapable of serious and intelligent compromises over a path out of our mess, we are likely to choose the least thoughtful and most disruptive path of the fiscal cliff. Yet should we go over the cliff we likely continue to have a deficit of over half a trillion dollars (assuming interest rates remain low) due to the sheer size of the problem. Maybe after going over the cliff our voter-elected partisan leaders will get down to actually figuring out some compromises.

If only there was a "nose in the book penalty" for our politicians who refuse to compromise...

Subscribe to:

Posts (Atom)