Vanishing Point - In art, the point on the horizon line at which

any two or more parallel lines seem to meet.

For this article, the space between the two lines represents the road of Quantitative Easing with price stability, the space to the left - deflation, and the space to the right - inflation. The longer the Federal reserve extends QE into the future, the harder it becomes to maintain price stability, ultimately proving unsustainable at the vanishing point. Our position remains fixed as we watch the Fed drive down the road.

Deflationary - Commodities, Wage-Price

Neutral - Currency, Fiat, Good and Services

Inflationary - Financial Assets, Tangible Assets

In this entry I again borrow the framework developed by A. Gary Schilling on inflation to breakdown the trends and hopefully glean a bit more insight into the future. His framework breaks down inflationary/ deflationary pressures into seven areas, which are commodity, wage-price, financial assets, tangible assets, currency, fiat, and goods and services.

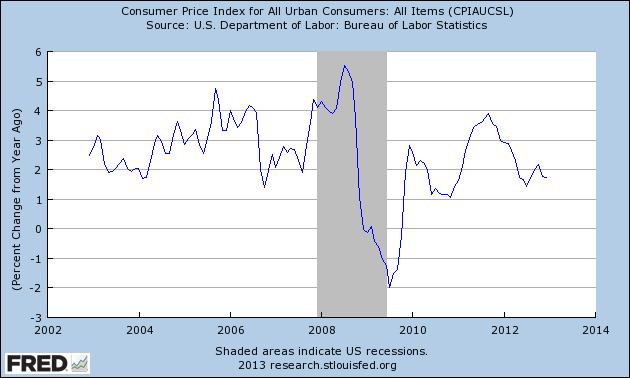

Commodity - Deflationary

Wage-Price - Deflationary, but Possibly Recovering

If income growth is flat-to-down, then the only way demand for goods and services can increase is if either debt levels go up (savings go down), or prices go down. Not surprisingly, the radio station WBUR highlighted that breaks in income streams has increasingly contributed to greater financial difficulty amongst consumers.

Indeed, total consumer credit has steadily increased over the past couple years. The main driver of the growth in consumer credit is non-revolving credit, for credit for categories like automobiles, education. As total credit per capita increases, and income remains stagnant, the purchasing power of the consumer declines unless interest rates continue to decline. Alternatively, for a period of time consumption can continue if asset prices are increasing, enabling cash infusions from rising equity in homes and other assets. While debt continues to rise, I believe we are nearing the end game of both falling interest rates and rising home equity.

Financial Assets - Inflationary

Tangible Assets - Inflationary

House prices have been rising, and expectations about the rate of growth have been rising over the six months. This rise in expectations is likely the direct result of the Federal reserve purchasing mortgage-backed securities, pushing mortgage rates lower. Lower rates mean a person can afford to pay more for a house with the same income level. If banks loosen lending standards then the trend in housing prices may accelerate higher as another housing bubble is inflated.

If major banks like Bank of America begin to aggressively go after new lending business then this category may provide a major inflationary force in the economy as banks draw down reserves in order to make loans, increasing the money multiplier and thus the amount of money in circulation.

Currency - Neutral

The US dollar continues to hold up fairly well relative to most other major currencies. This resilience is largely due to the aggressive monetary policies by most foreign central banks, although there is some puzzlement. In addition, the large reserves held by banks has so far reduced the multiplier effect, and thus the actual amount of money in circulation is not nearly as high as the potential. The potential inflationary force of a weaker dollar is likely held in check so long as the US dollar holds its value relative to other major currencies and banks remain conservative with their reserves.

How the debate about the overall role of government plays out likely determines whether this swings inflationary or deflationary. If the gridlock has accomplished anything, it has allowed the status quo to remain in place, neither applying further inflationary pressures through growing deficits nor swinging to deflationary pressures through austerity measures.

Clearly the Republicans prefer the road of austerity through reduced spending, although have accepted limited tax increases to avoid the "fiscal cliff." As we have seen in Europe, this path likely causes an economic slowdown in the near-term with deflationary forces. The Democrats don't want to cut spending and seem a little more accepting of deficit spending in order to spur economic growth, although higher taxes are clearly a part of their argument.

Across the Pacific is Japan, which has pursued endless rounds of stimulus to drive economic growth, only to pile national debt up to 2.5x GDP. Japan has been described as "a fly looking for a windshield," splat is only a matter of time with an aging population and mounting debt. Across the Atlantic is Europe, which has been taking its medicine through more austere measures and seen GDP growth fall. So long as the social and political structures remain in place, Europe should emerge stronger in the long run after a painful retrenchment.

If the "grand bargain" becomes additional higher taxes coupled with lower spending, then this segment swings definitively deflationary. If spending is not cut, and even increased to stimulate the economy, then this segment applies inflationary forces to the economy. More than likely, since the deficit has been trending down, the government agrees on moderate spending cuts. Simply reducing the spending on the war effort should be considered deflationary. Of course, Congress may not increase the debt ceiling and federal spending in indiscriminately and severely cut.

Goods and Services - Neutral

The combination of flat income and rising non-revolving debt balances leaves weaker consumer spending on items typically purchased with credit cards, either discretionary or non-discretionary. It is possible that more aggressive mortgage lending practices by banks may enable home prices to rise, thus providing home owners with larger equity balances with which to spend on goods and services. However, I fear that driver would only lead to another economic shock as US consumers are already tapping 401k balances to pay monthly bills.

Has the supply of retail declined, thus enabling a rise in prices due to lessening competition? The answer is simply "no." If anything, the American consumer remains over-supplied with stores, as highlighted by the recent weakness in retail REITs focused on strip malls. This over-supply of retail outlets reduces pricing power amongst retailers and provides a deflationary force to the economy. Lower mortgage payments through re-financing and tepid economic growth have so far kept the supply-demand dynamics in balance.

AIER's EPI - Everyday Price Index