There is little doubt the Federal Reserve's quantitative easing policy has helped bolster asset prices, especially prices for bonds, equity and houses. The U.S. stock markets sit around record highs, treasury yields are near record lows, and interest rates on mortgages are near record lows. These factors have created a "wealth effect" in which owners of these assets feel better off.

The question is: Does this asset appreciation mean we reach an "escape velocity" for the economy or does it set us up for greater volatility (ie. another burst bubble)?

Time will prove the fairest judge of this debate. But for now, maybe the biggest long lasting impact of recent monetary policy has been in the area of academia. Through Mr. Bernanke's tinkering we are learning about the limitations of monetary policy. It is becoming apparent that monetary policy has a direct impact on asset prices but the impact on labor markets and consumer spending is more indirect, and potentially dominated by other factors. Similar to a whip, Bernanke applies force to one end with the expectation of a "crack" at the other end. Will the monetary force used to lift asset prices result in a Bernanke-Jones whip-like economic snap or a Bernanke-Tube Man violation?

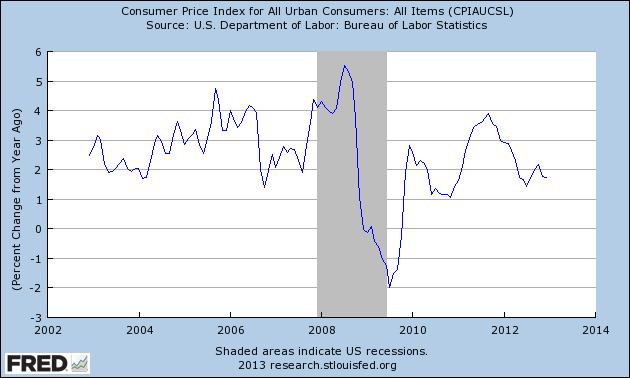

The declining velocity of money and slowing growth in the money supply suggest more of a tube man blowing hot hair than Indiana Jones getting the treasure (and girl). Slowing velocity and slowing monetary base growth equals slowing nominal GDP. In other words, inflation risk is declining and deflation risk is increasing, supported by weak gold prices and TIPS.

Recent economic releases continue to paint a mixed economic picture. Consumer spending appears weakening, with cash-register sales declining 0.4% in March. Consumer sentiment fell to the lowest level in nine months. Retailers are actually cutting jobs. The reasons for this weakness are varied, including rising healthcare costs consuming more of a family's budget, rising income taxes, falling mortgage refinancing activity as rates have been at a prolonged nadir, and federal sequestration.

The recent weakness in bank earnings, and the nearing end of lowering loan-loss reserves to bolster earnings, may provide a clearer picture of the strength of the economy. In an ultra low long-term rate environment it is challenging for financial companies to produce acceptable returns. Even more concerning, a research article by Robert C. Merton highlights that due to explicit and implicit government guarantees bank earnings face a "doubly convex" curve, masking the real risk to banks' earnings when the economy worsens and increasing economic volatility. So what seems like satisfactory risk controls in a normal environment can quickly deteriorate into a crisis during an economic downturn.

Central banks are raising the stakes in their battle to drive economic growth, a notion that should cause more skepticism. Most recently, Japan's central bank has committed to expand its balance sheet through asset purchases at the rate of 1% of GDP each month, potentially doubling the base money within two years. This policy is expected to continue for as long as necessary. All of this to offset a naturally deflationary environment caused by an aging population and a relatively inflexible economy. Are central banks lifting us to a recovery or simply holding on as more weight is added to a recession scenario?

Rising prices are not a major contributor with most commodity prices flat to down, including major influences like gasoline and food. Countries that have traditionally relied on commodity exports have been experiencing weakness, including Canada and Chile. In fact, with a consumer debt level to disposable income at a record level of 165% and oil revenue $6 billion below expectations, there is growing concern in Canada that the economy will continue to weaken.

In an environment in which some have characterized as a "no bad news" environment for markets, there is a deep fundamental belief that the monetary policy can cure all. In a perverse way, bad labor market statistics actually encourage the markets because the likelihood of the Fed extending its easing stance increases. Great for the asset markets but maybe not as much so for the economy, especially when growing risks of price destabilization, either inflationary or deflationary, are considered

The markets continue to skip down the path paved by the Bernanke-the-wizard's dollars. Take away that dollar-covered curtain and the picture is down right scary.